Spend a few minutes talking with neighbors around the North St. Charles area, and a common theme starts to emerge: “My housing costs keep going up…”

Historically, that usually meant rising mortgage rates or rents. Yet right now, that’s not the full story. Housing activity is picking up again, but local data reveals a more nuanced picture.

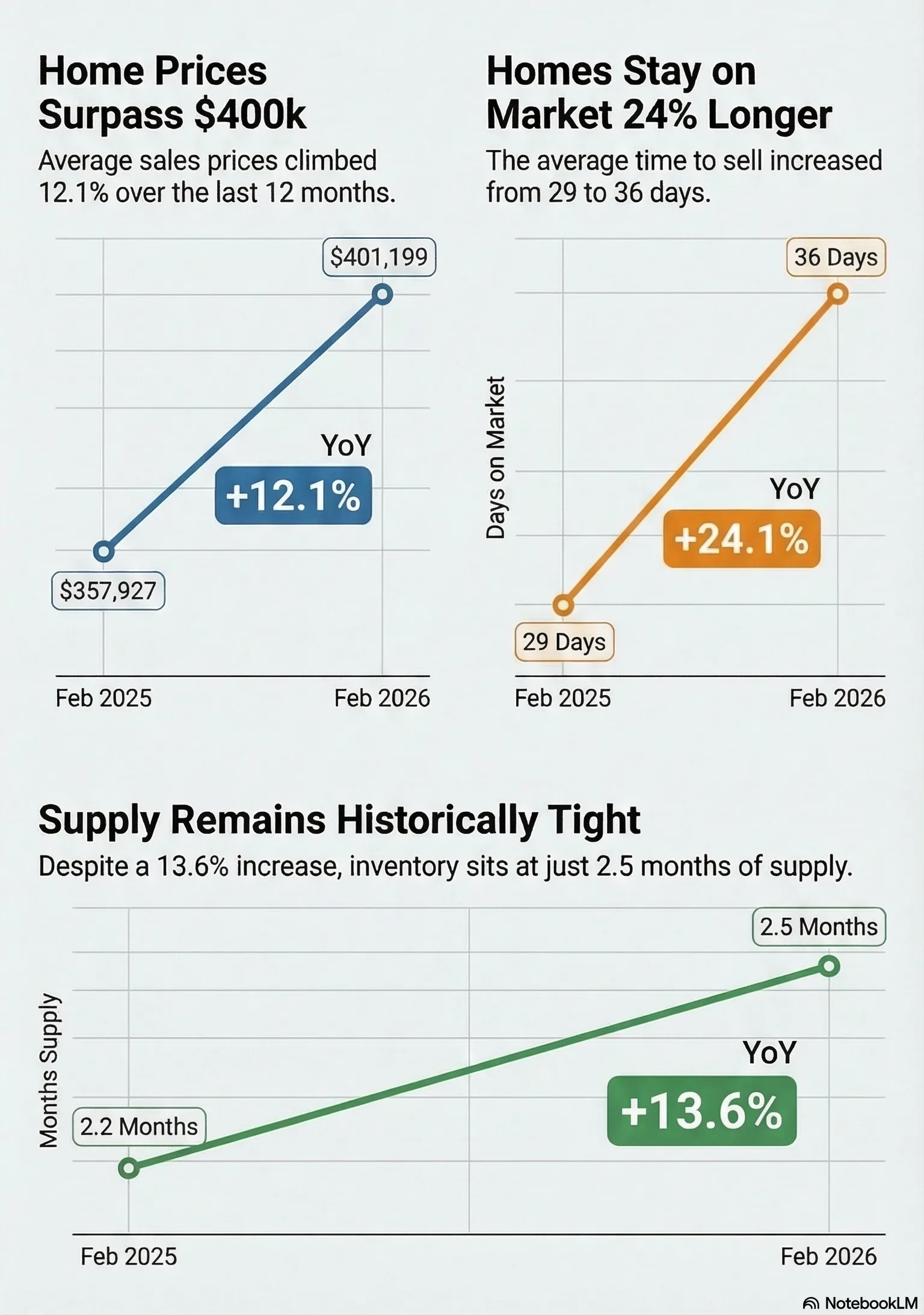

Over the past 12 months, home prices in the Orchard Farm School District have increased by more than 10% year over year. At the same time, closed sales are up roughly 15–20%, showing that buyers remain active and demand is strong.

However, the pace has shifted. Homes are taking longer to sell—days on market are up more than 20% year over year—and inventory has increased modestly. Even so, supply remains tight, hovering around 2–3 months, well below what’s considered a balanced market.

Industry professionals measure this using the absorption rate, or how quickly homes are selling relative to available supply. Even with a slight increase in inventory, Orchard Farm continues to operate in a range that reflects strong demand and steady turnover, not a slowing market. In other words, the market hasn’t weakened—it’s matured.

Why Does It Feel Harder?

The cost of owning—and buying—a home is rising in ways that don’t always make headlines. As home values increase, property taxes follow. At the same time, homeowners insurance has become one of the fastest-growing expenses. Many local homeowners have seen insurance costs increase 40% or more in recent years, with continued upward pressure tied to rebuild costs, claims, and overall risk.

“What people are experiencing isn’t a change in their mortgage—it’s everything around it,” said Jeff Flowerree, a local insurance agent. “Insurance costs have been rising due to rebuild costs, claims, and overall risk. It’s not a short-term issue—it’s something homeowners need to plan for going forward.”

These increases are often rolled into escrow, meaning even homeowners with fixed-rate loans are seeing their monthly payments rise—sometimes by a few hundred dollars depending on tax and insurance changes.

Rising Costs for Home Buyers

For home buyers, the pressure starts even earlier. Closing costs—often overlooked until the final stages—are also increasing. New federal reporting requirements tied to anti-money laundering rules are adding steps to closings, particularly for certain types of purchases.

“We’re seeing closing costs increase across the board,” said John Duckworth, President of True Title Company. “Between compliance requirements and processing, it’s adding roughly $150 to $500 per transaction, and overall fees are up 6–7% or more in many cases.”

Even the cost of qualifying for a mortgage is rising. The cost lenders pay for consumer credit reports has increased significantly—often doubling or more, adding $100 to $250+ per borrower to the loan process. Local lender Mark Gorman notes these are costs buyers rarely anticipate.

“These are behind-the-scenes costs, but they’re real,” Gorman said. “When you combine credit report increases with higher insurance, taxes, and closing costs, it all adds up for the buyer.”

New Construction and Affordability Pressures

New Town and the surrounding community have long benefited from new home development, but builders are now facing affordability pressures of their own. Higher material costs, labor constraints, and buyer sensitivity to pricing are making it harder to deliver new homes at entry-level price points. This can slow new supply and keep overall inventory tight, even as demand remains steady.

All of this is contributing to a subtle but important shift in the market. Higher-end homes are still moving, while affordability pressure is more noticeable at lower price points, making buyers more selective. Local property tax relief—including tax freezes—adds complexity by slowing tax revenue growth, reducing housing turnover, and tightening supply, putting pressure on entry-level housing.

That’s where the Orchard Farm story begins to diverge from the national narrative.

The Bottom Line

The market is still strong. Prices are rising. Buyers are active. But the cost of participating—from monthly payments to closing day—is higher than many expect. And that’s why, even in a healthy market, it feels different this time.